The Top 4 Regrets In Retirement

Regardless of where you are in your working life, the idea of retirement probably crosses your mind regularly. It’s a milestone we often start thinking about as soon as we join the workforce and many of us relish the idea of slowing down, changing pace, and finally having all the time we need to pursue passions and invest in relationships.

But what happens when you get to retirement and it’s not all it’s cracked up to be? Have you considered the idea that you could regret your decision to retire? Here are four common retirement regrets to keep in mind as you prepare for your golden years.

1. Retiring Too Early

Whether you were forced to retire earlier than planned or you made the decision on your own, retiring before you are ready can cause plenty of regret. In fact, 30% of retirees admitted they would gladly re-enter the workforce if a job became available. (1)

If you decided to retire prior to turning 65, you probably had to find pre-Medicare coverage, which is often quite a bit more expensive than an employer-sponsored plan. By waiting until you turn 65, you will qualify for Medicare and not be forced to obtain other health insurance to cover you during the transition.

Financially, the earlier you retire the fewer years you have to save and the longer you will have to live off of your money. If your finances are keeping you up at night or you are living at a lower quality of life than you are used to, you may regret retiring when you did.

Working even a few years longer can provide these valuable benefits:

- More time to accumulate savings

- More years to apply towards Social Security which could result in a larger benefit amount

- Health insurance coverage through your employer

- Purpose and identity

- Stronger mental and physical health (2)

2. Not Claiming Social Security Properly

Social Security benefits can be claimed anytime between ages 62 and 70. However, the timing of when you choose to collect these benefits will impact the amount of benefit you receive.

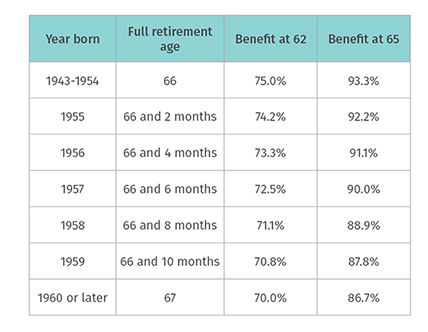

Full retirement age (FRA) changes based on the year you were born. For those born in 1937 and earlier, FRA is 65. After 1937, two months is added each year until FRA becomes 66 for those born between 1943 and 1954. Starting in 1955, two months a year is added again until the FRA becomes 67 for those born in 1960 or later.

If you wait until you reach full retirement age to begin collecting your Social Security benefits, you will receive your full Primary Insurance Amount, which is the full benefit that you have earned, but if you choose or are forced into an early retirement, you will receive a reduced benefit. Your basic benefit is reduced a fraction of a percent for each month you begin receiving benefits prior to full retirement age, up to 30%.

3. Overspending In The First Years Of Retirement

Even if you have a solid nest egg saved to carry you through retirement, you still need to exercise financial discipline to ensure your money lasts. Dipping too deep into your savings as soon as you retire could make or break your retirement dreams.

Instead, create a realistic retirement budget, factoring in travel or hobbies, then work with your advisor to find a withdrawal rate that will stretch your money for as long as possible.

4. Not Having A Retirement Bucket List

Free time is a major perk of retirement, but when you go from working full-time to not working at all it can be a shock to your system. Saying goodbye to your career, your colleagues, and your routines can cause anxiety and depression. But if you plan ahead to fill your time with activities that will fulfill you, you can avoid the negative emotions that can come with this life transition.

Do you want to know what activities result in a fulfilling retirement? A BMO study on retirement planning reveals that retirees who stayed busy and active, pursued independence, and volunteered their time were satisfied with their life. (3) One study of retirees even found that those who volunteered 200 hours a year were less likely to develop high blood pressure. (4)

The takeaway here is to be intentional about your time in retirement. Make a list of things you want to do, places you want to go, and people you want to spend time with, then strategically map out the details so your goals become a reality. It’s easy to lose your identity when you say goodbye to your career, but filling your time and venturing out into new territory will help you build a new identity and give you something to look forward to.

Live With No Regrets

You probably don’t want to celebrate the incredible milestone of retirement and then wake up the next day wondering if you made the right decision. Deciding when and how to retire is one of the most difficult decisions you will make in life, but you don’t have to make the hard choices alone. If you want to avoid facing these common regrets when you retire, reach out to us at 830-798-9400 or email smrosamond@rosamondfinancialgroup.com.

About Preston

Preston Rosamond is a financial advisor and the founder of The Rosamond Financial Group with nearly two decades of industry experience. He provides comprehensive wealth management and financial services to individuals, professionals, and families who enjoy simplicity and seek a professional to help them pursue their goals. Preston personally serves his clients with an individual touch and a sincere heart, and his servant’s attitude is evident from the moment you meet him. Learn more about Preston or start the conversation about your finances with him by emailing smrosamond@rosamondfinancialgroup.com.

_______

(1) https://www.cnbc.com/2014/08/21/retirees-go-back-to-work.html

(2) http://www.medicaldaily.com/planning-retiring-early-consider-these-5-health-risks-first-247669

(3) https://commercial.bmoharris.com/resource/wealth-management/whats-your-retirement-game-plan/

(4) http://psycnet.apa.org/journals/pag/28/2/578/?_ga=1.177767717.1281536077.1488342343